Da-Cook

Written by Nick Ackerman, co-edited by Stanford Chemist. This article was originally published on July 22, 2022 for members of the CEF/ETF Income Lab.

BlackRock Science and Technology Trust (NYSE:BST) and BlackRock Science and Technology Trust II (NYSE:BSTZ) are two funds that I follow regularly. I own both, and have covered more of the fund’s fundamentals. In the previous article. I won’t cover that whole topic again. Instead, today we’ll look at a further update on how these funds have been performing.

One of the biggest differences is that BST typically invests in large, well-established companies. This difference becomes more pronounced as BST moves to more speculative names. Still, several large mega-cap names remain. That didn’t give much comfort to the fund, though, as it was experiencing strong losses.

Performance comparison

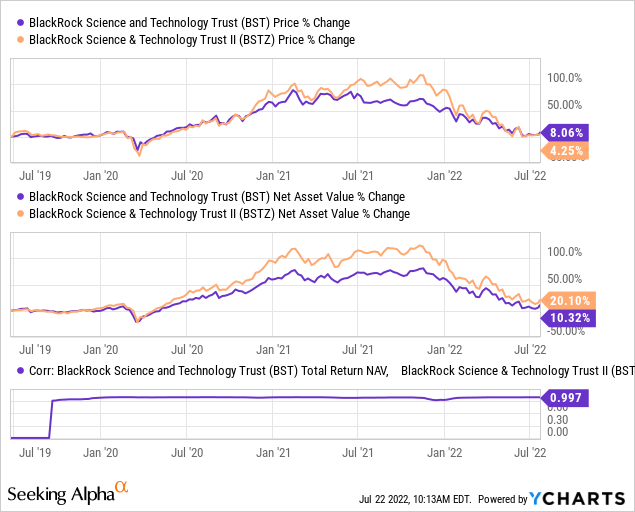

See the price and NAV performance of the fund since the launch of BSTZ. This chart does not show the effects of distribution (ie, it does not show total earnings.) The correlation coefficient is also provided, showing a significant correlation.

Ycharts

This differs from what we have seen in BlackGorg Health Sciences Trust (BME) and BlackGorg Health Sciences Trust II (BMEZ). In those funds, it was a material difference that resulted in a relatively more meaningful decline in correlation. For those two funds, we have provided examples where other funds have offered higher correlations.

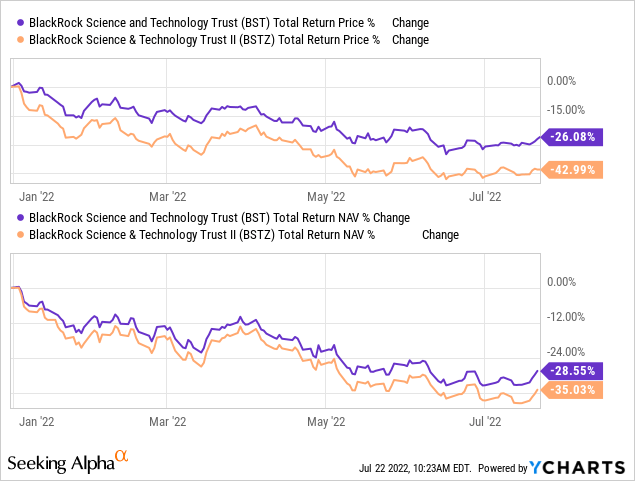

Coming back to BST and BSTZ, we can look at YTD performance. Both funds experienced some sharp losses in overall NAV returns. Total stock price returns diverge materially. That’s what offers the best opportunity to convert candidates.

Ycharts

In BSTZ’s case, the fund’s share price fell faster than the fund’s NAV return. Of course, this opens up a discount for the money. That’s exactly what we’re looking for when we want to invest in closed-end funds.

On the other hand, the BST share price has outperformed the NAV. This resulted in the opposite of what we wanted to see. It’s at least the opposite of what we’d want to see if we were looking to invest in a fund. It may be useful for existing shareholders in the fund.

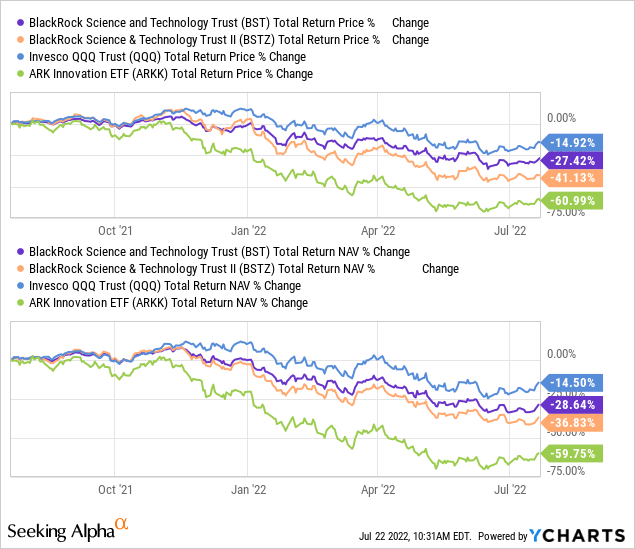

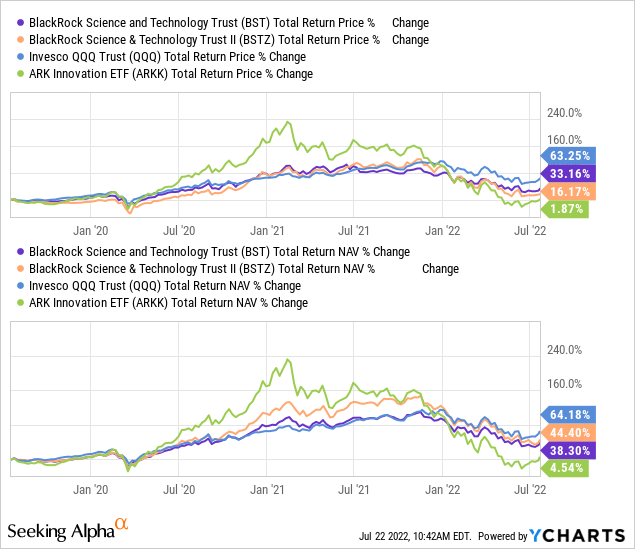

The last comparison I want to include is the relative performance of BST and BSTZ against some similar ETFs. For this we use Invesco QQQ (QQQ) – a proxy for the Nasdaq 100. We also use ARK Innovation (ARKK) because ARKK holds many small and speculative companies related to the BSTZ portfolio.

In this case, we can see that ARCK has done the worst by a long shot. We can also see that QQQ is holding relatively better thanks to its non-tech holdings.

Ycharts

Even going back, the decline in ARKK was so deep and rapid that BST and BSTZ still outperformed. Some of the defenses here may be due to the writing options that the funds perform. However, the biggest factor will be the overall position of the fund.

Ycharts

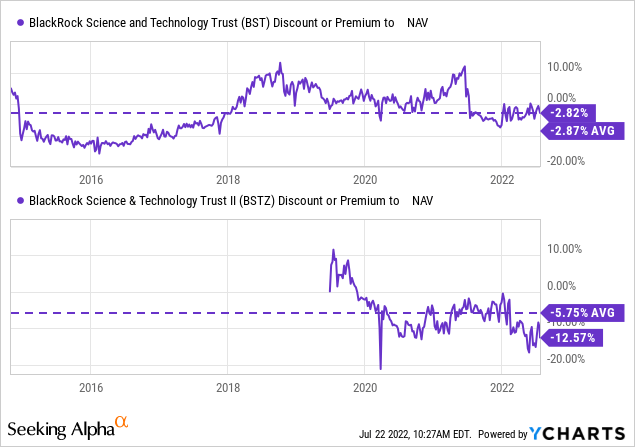

Discount comparison

BST has a longer history than BSTZ. In the year Going back to the beginning of 2014, BSTZ will start in 2019. That gives us a significantly lower track record for BSTZ when looking at discount history.

What history suggests is that BSTZ is a very compelling valuation at this point. BST is right next to its historical average. That doesn’t necessarily indicate a strong buy or strong sell, more hold or neutral rating. That being said, from shortly after the fund’s launch until around 2018, we can see the fund’s decline being rather continuous.

Ycharts

Distributions allow attractive payments from tech

Historically, technology has not been an area of high returns for investors. In the case of BST and BSTZ, the results of the CEF structure allow monthly distributions from these funds. The distributions can come in the form of earnings, income and return of capital. Neither of these funds have a positive net investment income figure, meaning they rely entirely on capital gains or returns on capital.

Both BST and BSTZ distributions were classified as long-term capital gains in 2021. This year’s official tax figures will not be known until the end of the year. Given the direction and challenges of the market, we would not be surprised to see capital in their distribution.

While it may be difficult to capitalize on the technology selloff that continues to drive these currencies lower and lower, all hope is not lost. They have built-in capital gains that they can continue to use. At the end of 2021, BSTZ had over $1.5 billion in unrealized profits, and BST had nearly $886 million in unrealized profits. These figures would fall at this point, the losses in the underlying portfolios will continue.

Even though everything related to technology is selling, you can still make a profit by buying low and selling high. Often, this is not the case with CEFs, as that requires more active management.

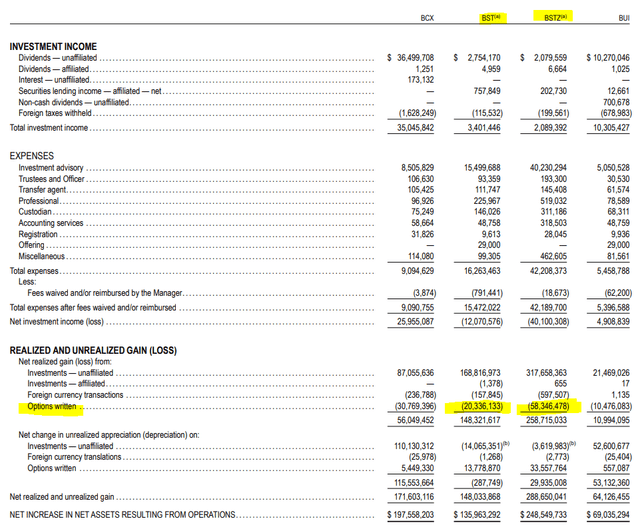

Additionally, this is where an options strategy can come in handy. Typically, covered call writing on individual names in the portfolio has resulted in losses for the fund. We could see this for both currencies in 2021. It wasn’t a huge loss for the size of these funds, but losses nonetheless.

Annual Report (BlackRock (Author’s Highlights))

This happens when they buy a position to close before they are called. But with the losses piling up this year, they don’t have to return positions to get out of the contract. This should provide guaranteed capital gains for the fund this year. That could offset some of the declines in the funds.

I believe both funds are at risk of a spread reduction if things don’t improve, as capital gains will be hard to come by. BSTZ is more vulnerable as the fund’s NAV spreads at 9.59%. For BST, they are at a dividend yield of 8.38% of NAV. Either way, these funds remain an attractive place to seek “income” from tech holdings, where tech typically pays low yields.

A look at the portfolios

BST

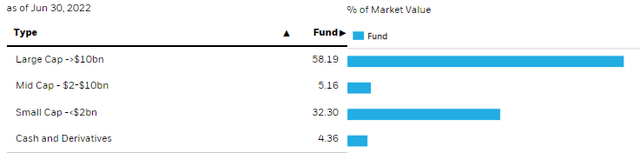

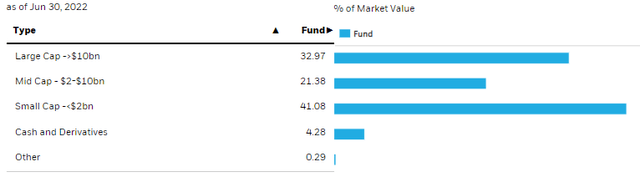

As mentioned earlier, BST typically carries large cap names. They are still moving more towards small-cap names. Here’s the latest showing a slight shift to small-cap names again. The average market value of their holdings is $581,353.9 million.

Presumably, some of these are the result of mid-cap or large-cap names falling to the small-cap level. It’s not too wild to think that some tech names have seen their stock prices drop 70% or more.

BST Market Cap Weight (BlackRock)

Small cap exposure has really increased over the past year. Looking at the previous June 2021 weighting, small-caps were only around 17% of the portfolio. Even before 2020, no project name has been released. The verdict is still out.

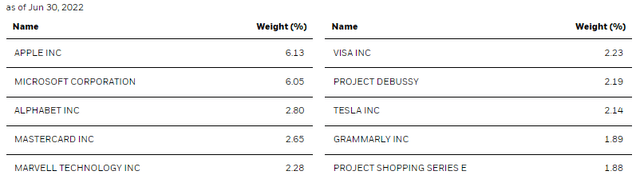

Looking at the top ten, we still hang on to names like Apple ( AAPL ), Microsoft ( MSFT ), and Alphabet ( GOOG ). However, we have two of the ten “project” names. Those are associated with private investments which are abundant in BSTZ.

BST Top Ten (Black Rock)

BSTZ

Looking at BSTZ, we still see a higher relative weight to small caps, and mid caps also form a meaningful allocation. Large-cap weightage was previously around 52% of the fund. A significant drop in technology is expected to provide some weight loss here as well. The average market value of BSTZ is about $53,454.1 million.

That’s a big difference from BST. It goes back to AAPL, MSFT, and GOOG, but these names have proportionately higher average market value of their core holdings. They are companies with a market capitalization of $1.5 to $2.5 trillion.

BSTZ Market Cap Weight (BlackRock)

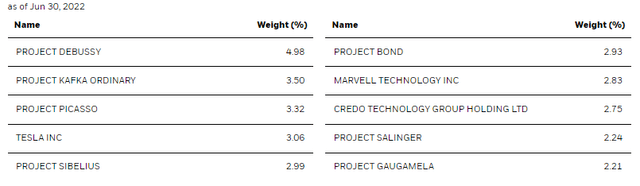

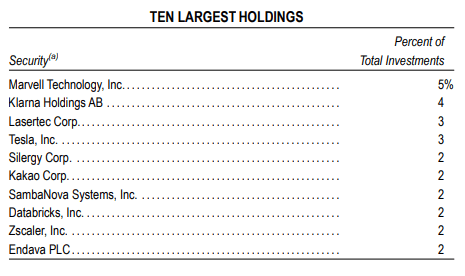

In terms of BSTZ’s top ten, we see some new project names. Again, these are their personal investment nicknames. Project Bond, Project Salinger, and Project Gaugamela from the previous BST/BSTZ piece are new additions to this list. Now we have seven names from the list of four project names at the beginning of the year. This was six earlier this year, as well, in my latest update on BSTZ. Project Gaugamela is the latest addition. They don’t have their second quarter criticism this time around.

BSTZ Top Ten Holdings (Black Rock)

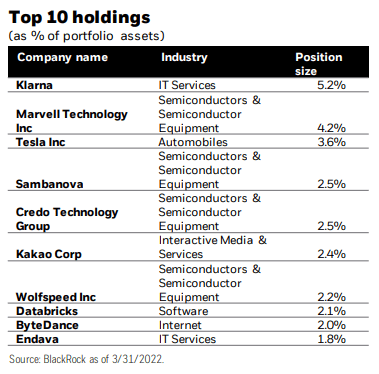

At the beginning of July, when Klarna (Project Kafka) raised a new round of cash, the valuation fell again. That suggests we will look to lower that position when they update the BSTZ.

BSTZ Top Ten 03/31/2022 (Black Rock)

Hide “project”.

If you want a clear, concise portfolio where you know what you’ve got. BSTZ probably not. I’ve done my best to test what some of these project names refer to. Klarna is easy, but they make it difficult.

One way I thought it would be easy to compare is when they list the holdings on their site and refer to their year-end annual report.

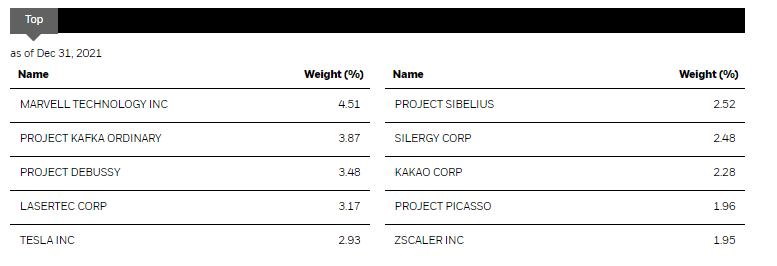

Here we take a snapshot of December 2021 holdings for BSTZ.

BSTZ Top Ten 12/31/2021 (Black Rock)

Go to the year-end report, which also has a December 31, 2021, reporting date, and that’s what we get.

BSTZ Top Ten 12/31/2021 (Black Rock)

What we see here is that the top ten holdings on their website aren’t really making sense because they are top ten “exposures” and not specific holdings.

See project congestion? That’s Databricks. How can it be? This is because they occupy three separate positions in the Databrick, with a value of $106,513,808 at the end of 2021. In terms of total net assets at that time, it works out to about 3.5% or closer to the 3.48% you listed.

However, the annual report shows that Databricks is listed as the eighth largest benchmark. That’s because they have one position – a Series F round for $62,212,977 – about 2.04%, or 2% of what they listed.

Conclusion

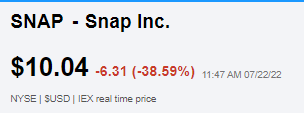

BST and BSTZ continue to crash into the inevitable tech selloff. At the time of this writing, Snap ( SNAP ) was reporting weak results and a 38.6% crash, but the technology doesn’t seem ready for a rebound yet.

SNAP Price 7/22 (Seeking Alpha)

These will be long-term positions in my portfolio. If I were working capital today, I would lean more towards BSTZ at a bigger discount. However, with heavy personal investments, the discount here may be more appropriate. Private investments can be limited, and the value is not known until they go to sell. One should be okay with this high risk proposition before investing in BSTZ.

BST continues its trend of investing in smaller companies by leaning towards the BSTZ position. This will either make them look like a genius in the end, or I’ll end up with two poor bucks.