Richard Drury/DigitalVision via Getty Images

Introduction

Although several large companies including Tencent (OTCPK: TCEHY ), Alibaba (BABA) and Ping An Insurance (OTCPK: PNGAY ) are operating in a tough environment posting big declines in EPS figures, NetEase’s (NASDAQ: NTES) fundamentals have remained stable. Since the stock is declining due to political issues and not due to weak earnings or prospects, I believe there is value to be found in NetEase.

NetEase is a Chinese company that provides online services focused on content, communication and business. The company is a developer and operator of several online PC and mobile games, email and advertising services. NetEase has licensing agreements with major companies including Mojang and Blizzard to bring some of their titles to the Chinese market.

The basics

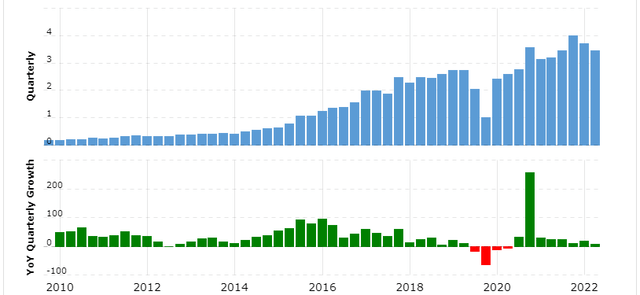

NetEase grew its revenue at a rapid pace, with only a few quarterly declines. In the year By 2010, it had grown by an average of 30 percent.

As the company grew, growth eventually dropped to low double digits, a respectable growth rate considering the company’s size.

Growth is mostly due to new games being released while existing games continue to grow. As the plays eventually mature and more revenue is needed to move the needle, revenue growth is expected to slow.

Analysts expect revenue growth to continue next year.

Macrotrends.com

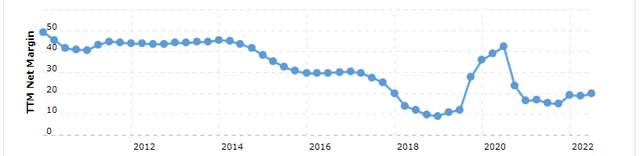

The profit margin shows a history of great profitability without a single year of negative earnings. However, after an explosive increase in revenue in 2015, the margin is decreasing, which is due to new games and licensing agreements.

After that it stabilized at ~17%.

Macrotrends.com

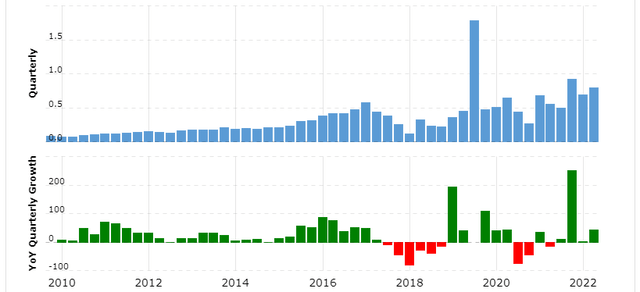

Rapid revenue growth, combined with a low but profitable profit margin, has resulted in several consecutive years of strong net income growth.

Net income growth has averaged ~21% annual growth from 2010 – 2022. The growth is impressive, especially when you consider it was achieved without diluting shareholders. The number of outstanding shares increased slightly, and thus EPS increased by ~20% year-over-year.

Macrotrends.com

Capital allocation

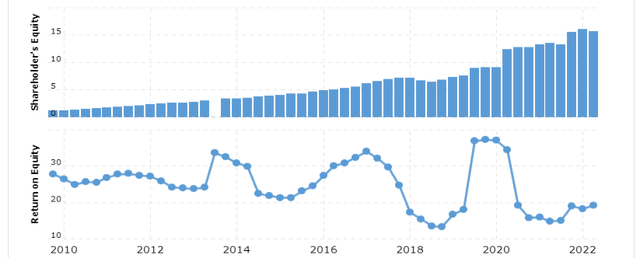

As shown in the image below, NetEase arrived at approx. 25% annual return on equity from 2010-2017. Considering that almost all earnings are reinvested, the returns are impressive. In the year Since 2013, only a small amount of income has been paid out in dividends, offsetting occasional small share buybacks.

Return on equity now looks stable at ~17%. As the company spends ~25% of earnings on dividends and reinvests 17% to maintain equity, equity and earnings should grow by ~12.75% annually.

The main takeaway is that the majority of earnings have been reinvested, which I believe is prudent given the high double-digit reinvestment rates that management can achieve.

I find it comforting that it seems to have stabilized and even increased in recent months. High reinvestment ability emphasizes the strength and power of the company.

Macrotrends.com

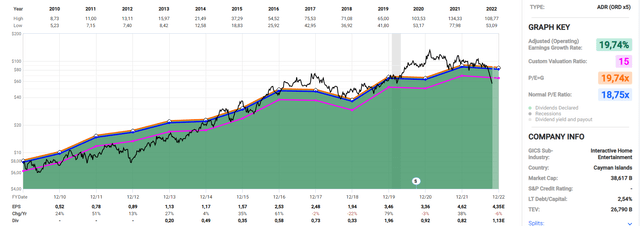

Price

As shown in the figure below, the average annual growth from 2010-2022 has reached 19.74 percent. We can also see that growth has slowed down in recent years. This was to be expected given the reduction in equity.

From 2010 – 2017, the annual growth in EPS was 25.05%. in line with their ROE during that period. Given that ROE was ~17% from 2017 – 2022 and a dividend payout ratio of ~25% with no meaningful share buybacks, a reasonable estimate of future EPS growth would be ~12.75%.

Estimated growth is in line with analysts’ expectations for the next 2 years, with low double digits expected.

The company has seen above-average growth over the past decade, and thus has been rewarded with a lot of above-normal earnings. Growth averaged 19.74% per year, and the average multiple was 18.75. Reversion to the mean multiple shows ~48% returns. I believe the company should be trading at a higher multiple than its current multiple of 12.9, but since it is unlikely to grow more than 15% annually, I do not believe the average multiple provides a margin of safety anymore.

A return to a standard 15 earnings multiple, which still represents ~20% downside potential, seems more reasonable.

Fastgraphs.com

Stock chart

A quick disclaimer: Technical analysis isn’t reason enough to buy a stock by itself, but when combined with a company’s fundamentals, it can significantly narrow your price range.

Shares of NetEase are currently below the 50-moving average, which has often been a strong support area in the past. This is typically seen with companies that are constantly growing, which NetEase assigns to. A return to the 50 moving average represents a 40% return. This brings the stock closer to the average multiple and slightly above the standard multiple of 15.

However, if the stock’s decline continues, which could be supported by market weakness in China and political developments, then I expect strong support at the 200 moving average. I think it’s highly unlikely that such low valuations would happen, but I guess anything is possible in this market.

Tradingview.com

Final thoughts

There is no doubt that NetEase is a strong business. The company has made significant progress on its fundamentals over the years, and it is not expected to stop anytime soon. Although the rate of reinvestment has decreased in recent years, it still shows promising prospects for future growth. With a 17% return on equity and a dividend yield of ~25%, an estimate of ~12.7% annual growth is very reasonable.

Considering the 12.7% annual growth, the current valuation looks very attractive. The company trades well below average earnings. I think it is somewhat justified by the low revenue growth, at least a standard multiple of 15 should be given going forward.

Although part of the lower valuation is due to political fears surrounding Chinese stocks, it is far from random, it is clear to see that NetEase has experienced less volatility than other Chinese stocks. The company expects only a slight decrease in EPS this year, after a year of +30% growth.

Barring political instability, the company is expected to grow in the double digits at a below-average earnings multiple. The stock chart is similar to the earnings in the opinion as it may be worth considering NetEase.

Therefore, I give the company a “buy” rating.